From Survive to Strategize: The Two Eras of Capital Raising at Provectus Biopharmaceuticals (PVCT)

There are two very different chapters in the capital markets and market capitalization history of Provectus Biopharmaceuticals:

Pre-2017, when there was dilution, distraction, and disarray, and

Post-2017, when new leadership’s goals have been alignment, structure, and strategy.

Before 2017, Provectus—despite owning a uniquely bioactive small molecule (rose bengal sodium, or RBS) with intriguing multi-indication potential (and really, really intriguing possibilities)—followed an errant path as a publicly-traded biotech company: rapid-fire equity raises, extensive warrant issuances, PIPEs with heavy discounting, no capital structure discipline, and an almost singular focus on a then-insufficiently understood or unrecognized stage of melanoma that left broader systems science superficially explored or altogether unexplored.

By the end of the pre-2017 era, capital was depleted, leadership credibility was destroyed, and scientific veracity was muddied and tarnished. Provectus stood at the brink of collapse. Most companies in this situation simply vanish. Shareholders are wiped out. Medical science is buried or, worse, lost forever.

Since 2017, a new team stepped in—not just to keep the lights on, but to realign the business:

Tranche-based structured financings to preserve flexibility and promote discipline,

Preferred equity with liquidation preferences to align incentives with success,

Subsidiary model (e.g., VisiRose for ophthalmology) to shield the parent from dilution, and,

Focused capital deployment based on immune and systems biology insights.

This wasn’t just a restart. It’s was a rebuild.

Yes, the Company’s current share price of ~9 cents is lower than 2024’s high of ~22 cents, albeit up from ~4 cents in April 2020 and from ~1 cent during Provectus’s final implosion in late-2016.

Longtime shareholders are still on the cap table—a rare situation given the Company’s pre-2017 trajectory. Many biotech stories don’t make it this far.

Understanding Dilution in Context

Let’s talk dilution—the word every long-term shareholder closely watches.

Since 2017, Provectus has raised over $34 million to re-establish operations to pursue an initial approval pathway of the Company’s intratumoral cancer immunotherapy PV-10 and to advance research into systemic immunological and other applications of RBS, while managing several challenging legacy aspects of the Company.

But what did that cost shareholders in terms of ownership?

2017 vs 2025 Cap Table Overview of Provectus

Key Insights:

Despite raising over $34 million, fully diluted shares outstanding increased just ~5% over 8 years.

Warrants phased out, while structured notes/preferred shares at a well-above stock market price became the primary vehicle to raise capital—significantly mitigating dilution.

Post-2017 fundraising hasn’t been unchecked dilution, like pre-2017. It has been controlled capitalization, designed to protect long-term shareholders from the very kind of fire-sale and death spiral financings that routinely destroy other micro-cap biotechnology companies.

2016 vs 2017 Cap Table Overview of Provectus

Key Insight:

The last capital raise by pre-2017 leadership, the so-called “ratchet raise” of 2016, netted ~$5.6 million (gross proceeds of $6 million), while contributing to an increase in fully diluted shares outstanding of more than 90% in only one year.

Furthermore, post-2017 new leadership shut down the pre-2017 team’s rights offering (i.e., the selling of rights to potential future Provectus drug sales) that prior leadership pursued shortly after the ratchet raise—an offering, which if completed, would have made the Company impossible to save.

Throughout its history prior to 2017, Provectus raised capital through the industry-standard (for micro-cap biotechnology companies) issuance of common stock with excessive warrant coverage amid high fees, particularly with one investment banking firm.

The post-2017 financing rounds at Provectus, all at ostensibly the same price, terms, and conditions, have been a mix of insider-like investments, led by people deeply involved with the Company’s new strategy and mission with “friends and family” characteristics given the relationship-based trust and private nature of the capital raised. These post-2017 capital raises, however, are neither insider nor friends-and-family in the true sense of these labels.

Provectus has raised investments at the price (28.62 cents per common share, as converted), terms, and conditions that new leadership originally set in March 2017 when it negotiated control of the Company from the prior board of directors.

Chairman and Chief Executive Officer Ed Pershing has continued to fund Provectus over the last couple of years, while continuing to pursue other sources of capital and investors. Of the more than $34 million of capital raised since 2017, Ed has invested ~$6.4 million in Provectus, including $3.6 million in 2022, ~$0.7 million in 2024, and ~$0.6 million in 2025 to date. Executive officers and the post-2017 members of the board of directors continue to accrue their compensation, converting some into equity at a well-above stock market price. We manage the Company’s cash burn and monthly spend as prudently as we can to remain in the game.

To that end, whose science would you want: pre-2017’s or what Provectus has to offer today?

Because We’re Still Here. Still Building. Still Aligned.

One thing that sets Provectus apart isn’t just science—it’s persistence.

Through board, executive, staff, and vendor turnover, capital restructuring, hard decisions, and other challenges, we’re still here. We didn’t go private. We didn’t go dark. We didn’t dissolve. We didn’t reverse-split common shareholders into oblivion.

Longtime shareholders are still on the cap table—a near-miracle in the micro-cap biotech world where most companies facing what Provectus did in 2016 would no longer exist.

Why? Because the focus hasn’t been on surviving the stock—it’s been on proving the science. RBS isn’t a hope story. It’s a systems-based, multi-indication therapeutic platform that’s being validated across immuno-oncology, ophthalmology, and dermatology, to name just a few disease areas being investigated.

When the science delivers—and we believe it will—the outcome won’t just be academic. We believe it will be transformational, medically for patients and financially for shareholders.

We’re trying to turn long-term shareholders from writing off their holdings in Provectus towards considering there could be a reasonably objective risk-reward opportunity for their prior investments.

That’s why everything we’ve done since 2017 has been about positioning for longevity, not price movement. Structure before splash. Value before visibility. And eventually—NASDAQ before noise. Because when that moment comes, we want everyone who believed early to still have their seat at the cap table.

A reverse split/reduction in authorized shares by the same ratio

Consider our prior requests of shareholders for a reverse stock split (e.g., 1-for-10, 1-for-20, 1-for-50) and a reduction in authorized shares by the same reverse split ratio.

What Does It Mean?

When a company asks shareholders to authorize both, it’s not just doing cosmetic housekeeping. It’s sending a message: “We are not using the reverse split to expand dilution capacity—we’re using it to clean up the capital structure.”

Why This Is Unusual—but Shareholder-Friendly

In most reverse stock splits, companies keep the pre-split authorized share count unchanged, which increases their post-split flexibility to issue more shares—often interpreted, oftentimes accurately, as a setup for future dilution.

But if a company reduces its authorized shares proportionally, it’s essentially not creating any new dilution runway. We believe that suggests no intent to flood the market post-split, no hidden shelf registration coming, and a desire to align optics with real discipline.

Strategic Interpretations

Caveats

A reverse split is still a reverse split—and the market tends to punish those unless there’s a catalyst: clinical or regulatory validation, institutional buy-in, and/or NASDAQ up-listing, for example.

We believe coupling the reverse split with a proportional reduction in authorized shares, at the right time, under the right circumstances, dramatically improves the narrative. It becomes not just a cosmetic reset, but a structural realignment.

Final Thought

We believe a company that pursues a reverse split with a matching reduction in authorized shares isn’t signaling dilution—it’s signaling discipline. In a market where trust can be scarce, that’s a rare—and often under-appreciated—move.

Addressing the Critics—With Clarity, Conviction, and Long-Term Perspective

We’ve heard the questions. We’ve seen the comments. And as a company that believes in long science and aligned value creation, we’re not afraid of hard conversations.

Since 2017, Provectus has chosen the road less traveled in biotech: Not price-chasing. Not visibility-chasing. But platform-building—with the integrity and intentionality it demands.

That doesn’t mean there haven’t been critiques. There have. Many of them fair.

Here are the “Top 10” criticisms we’ve heard—and how we see them.

Still on the OTCQB

We agree it limits visibility. But trying to up-list, if we could at all, without structural readiness is cosmetic. We’re not up-listing to spike. We’re up-listing to last.

No Big-Name Partnerships Yet

True. As we’ve noted in the past, we have had conversations under CDA with Big Pharma and received some good feedback. We’re building leverage, and potential future value, not just chasing validation.

Quiet in the Public Markets

Yes. Because when your story is built on substance, you don’t need to shout. We’ll boldly speak when it moves the market—and we’ll do our best to keep shareholders updated in the interim.

Capital Deployment Has Been Cautious

By design. We were entrusted with capital post-crisis as we conducted capital raises. Every dollar was and remains a vote of confidence—by non-related parties in us and our strategy, and by related parties like us in Provectus as we’ve built and continue to build it—and we’ve spent this money like it matters.

Preferred Shares Are Latently Dilutive

Only if we succeed. That’s the point. If value is created, conversion happens. We believe that’s upside alignment for preferred and common stockholders alike.

Share Price Hasn’t Moved

True, in context. But price doesn’t equal value—not here, not yet. We’re not building a penny stock. We’re building a platform company for the NASDAQ.

Visibility Moments Were Missed

We disagree. We deferred visibility to match real inflection points. Our goal is durable attention—not passing press cycles.

Trial Velocity Is Modest

Yes. Because RBS isn’t a single-target, single-path molecule. Far from it. It’s complex, and it requires smart science and smart clinical deployment—not fast headlines. Clinical trials are very expensive, and the Company cannot afford a miss (e.g., a poorly designed study that underutilizes PV-10 that doesn’t reflect PV-10’s true capacity to heal a patient from their disease).

No Commercialization Yet

Because we’re not a consumer biotech. But with Provectus situated as it is and with VisiRose and potentially future subsidiaries, approval pathways can be realistically formulated.

No Institutional Capital Participation

Not yet. But when data converges with delivery, institutions won’t be invited—they’ll be compelled.

Final Thought

We didn’t rebuild Provectus to survive a cycle. We rebuilt it to change medical care, and the way people think about drug discovery, immune modulation, and systems medicine. We’re not chasing critics. We’re building for the moment they change their tune.

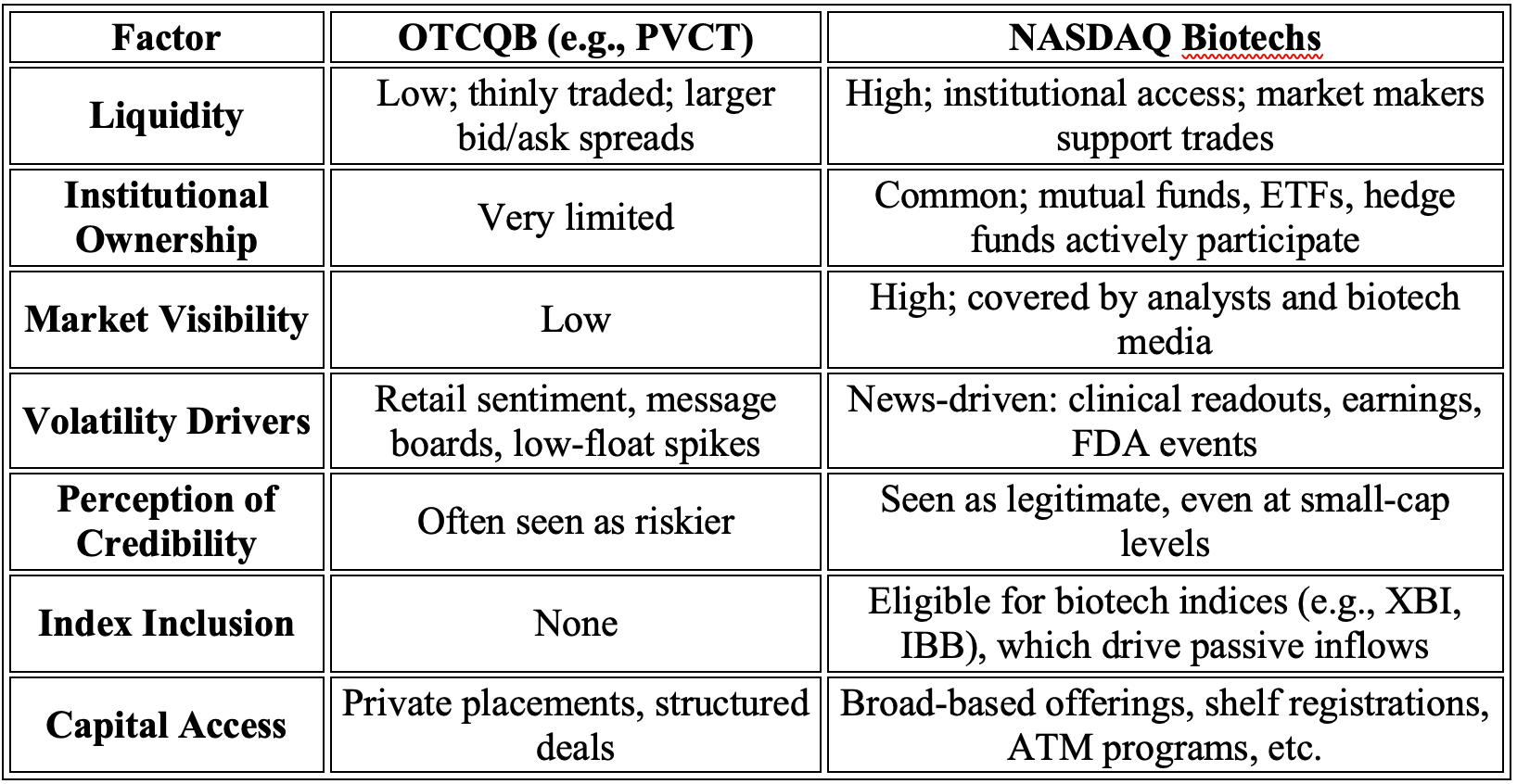

Where We Trade

It’s essential to understand the context of OTCQB trading when evaluating the relevance of PVCT’s share price action versus NASDAQ-listed biotech companies.

What Is the OTCQB?

The OTCQB (Venture Market) is one of the three tiers of the over-the-counter market in the U.S., sitting between the less regulated OTC Pink and the more reputable OTCQX. Companies on the OTCQB must be current in SEC reporting, are audited annually, and cannot be in bankruptcy.

PVCT is compliant, but OTCQB is still a materially different ecosystem than the NASDAQ.

Price Action: OTCQB vs. NASDAQ Biotechs

Why PVCT Price Action May Be Less “Serious”

Volume is low: A single trade can move the price disproportionately.

Institutional price discovery is absent: There’s no analyst coverage or indexed benchmark that tethers value to fundamentals.

Retail micro-cap behavior dominates: OTC trades are heavily influenced by sentiment and short-term speculation—not fundamentals or clinical milestones.

Why PVCT Still Matters

Because price ≠ value, especially on the OTCQB.

The real indicators of PVCT’s trajectory include:

Advancement of clinical and preclinical programs,

Strategic financings with aligned terms (e.g., liquidation preference),

Subsidiary commercialization pathways (e.g., VisiRose), and

Potential future up-listing (e.g., NASDAQ), which would reset the visibility, liquidity, and valuation dynamics.

Final Thought

PVCT’s current share price on the OTCQB should not be viewed as a serious proxy for intrinsic value or scientific progress. It reflects a thin market, not a verdict. As with many developmental-stage biotech companies, true value tends to emerge in punctuated milestones—not in daily ticks.

Forward-Looking Statements

The information provided in this Provectus Substack Post may include forward-looking statements, within the meaning of the Private Securities Litigation Reform Act of 1995, relating to the business of Provectus and its affiliates, which are based on currently available information and current assumptions, expectations, and projections about future events and are subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those projected in the forward-looking statements. Such statements are made in reliance on the safe harbor provisions of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Forward-looking statements are often, but not always, identified by the use of words such as “aim,” “likely,” “outlook,” “seek,” “anticipate,” “budget,” “plan,” “continue,” “estimate,” “expect,” “forecast,” “may,” “will,” “would,” “project,” “projection,” “predict,” “potential,” “targeting,” “intend,” “can,” “could,” “might,” “should,” “believe,” and similar words suggesting future outcomes or statements regarding an outlook.

The safety and efficacy of Provectus’s drug agents and/or their uses under investigation have not been established. There is no guarantee that the agents will receive health authority approval or become commercially available in any country for the uses being investigated or that such agents as products will achieve any revenue levels.

Due to the risks, uncertainties, and assumptions inherent in forward-looking statements, readers should not place undue reliance on these forward-looking statements. The forward-looking statements contained in this Provectus Substack Post are made as of the date hereof or as of the date specifically specified herein, and the Company undertakes no obligation to update or revise any forward-looking statements, whether because of new information, future events, or otherwise, except in accordance with applicable securities laws. The forward-looking statements are expressly qualified by this cautionary statement.

Risks, uncertainties, and assumptions include those discussed in the Company’s filings with the U.S. Securities and Exchange Commission, including those described in Item 1A of Provectus’ Annual Report on Form 10-K for the period ended December 31, 2024.